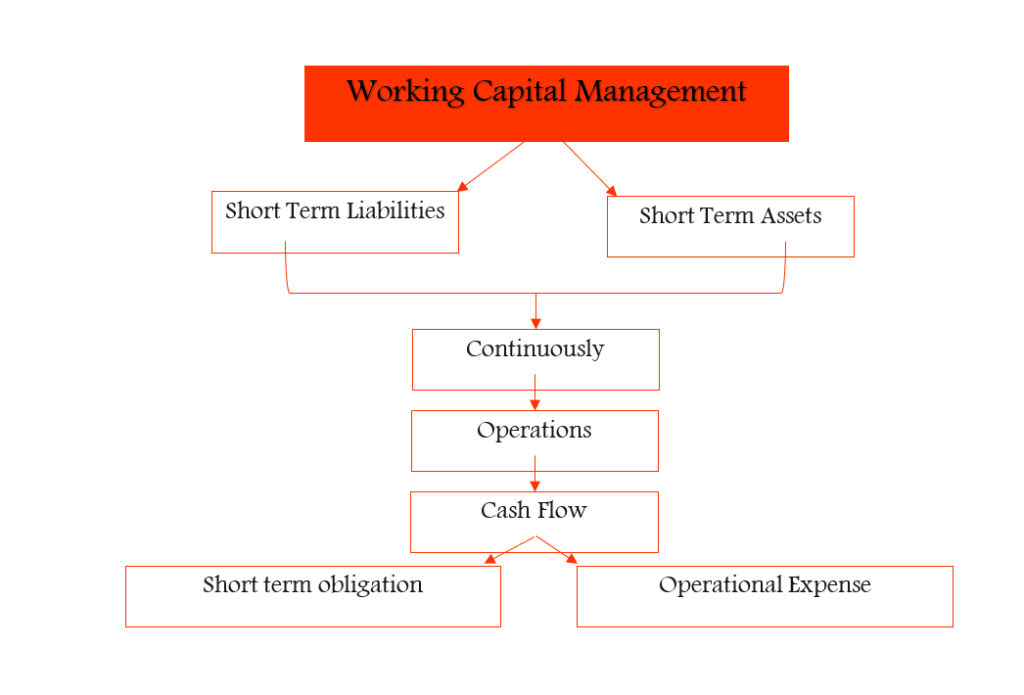

Working capital is the fund available for daily operations, crucial for purchasing raw materials, paying wages, salaries, rents, and managing day-to-day expenditures. It is also called circulating, revolving, floating, or liquid capital.

Key Reasons Businesses Fail.

- 5%: Marketing issues, competition, technology, quality, pricing, legal issues.

- 95%: Financial mismanagement related to working capital.

Components of Working Capital

♟️ Current Assets:

- Assets expected to be realized or consumed within 12 months or during the operating cycle.

- Examples: Inventory, receivables, cash/cash equivalents, prepaid expenses.

♟️ Current Liabilities:

- Liabilities are expected to be settled within 12 months or an operating cycle.

- Examples: Payables, outstanding wages, salaries.

Concepts of Working Capital

Working capital represents the short-term financial health of a business, highlighting its ability to cover immediate liabilities with available assets.

- Gross Concept: Total current assets.

- Net Concept: Excess of current assets over current liabilities.

- Working Capital Management:The administration of the firm’s current assets and the financing needed to support current assets.

Adequate Working Capital

Adequate working capital helps a business cover its short-term expenses, run smoothly, and handle unexpected costs.

| EXCESS WORKING CAPITAL | DEFICIT WORKING CAPITAL |

| Unnecessary Accumulation Of Inventory | Difficult Implement Operating Plan |

| Wastage | Cannot Achieve Profit Goal |

| Idle Fund | Cannot Meet Day To Day Obligations |

| Defective Credit Policy | Return On Investment Fall Due To The Under Utilisation Of Fixed Asset |

| Overall In-efficiency | Lost Credit Facility |

| Reputation & Goodwill Affect badly |

Importance of Working Capital Management

- Significant investment in current assets (50%-70% in manufacturing firms).

- No alternatives for current assets, unlike fixed assets that can be leased.

- Direct correlation between sales and current assets.

- Requires continuous monitoring to balance liquidity and efficiency.

Strategies for Managing Working Capital

- Hedging Approach: Long-term funds for permanent needs; short-term funds for temporary needs.

- Conservative Approach: Long-term funds for all needs, with short-term funds for emergencies.

- Aggressive Approach: Reliance on short-term funds.

- Zero WC Approach: Balancing current assets and liabilities.

Significance of Working Capital Management

1. Balancing Working Capital

- Adequate working capital is essential for smooth business operations.

- Excess working capital means idle funds, leading to high interest costs.

- Insufficient working capital increases the risk of insolvency, as liabilities may go unmet.

2. Short-Term and Long-Term Importance

- Working capital ensures liquidity for short-term needs.

- Sufficient liquidity is critical for long-term survival and growth.

3. Impact on Investment Decisions

- Investments in assets like machinery or buildings also require additional working capital.

- Example: Increased production needs more raw materials and inventory.

- Increased sales often lead to higher debtors (accounts receivable).

- Expansion in operations generally demands higher working capital.

4. Determining Optimum Working Capital

- The finance manager must estimate and maintain the right level of working capital.

- A current ratio of 2 (current assets/current liabilities) is ideal for manufacturing firms.

- An acid-test ratio (quick assets/current liabilities) of 1 ensures liquidity.

- These ratios serve as general benchmarks for financial stability.

5. Flexibility in Ratios

- Specific circumstances affect optimum working capital:

- If inventories are quickly sellable or debtors are like liquid cash, lower ratios may still indicate financial health.

6. Objectives of Working Capital Management

- Maintain adequate working capital.

- Ensure proper financing of working capital.

- Manage risks, returns, and share prices effectively.

7. Stakeholder Interest

- Bankers, financial analysts, investors, and institutions rely on these benchmarks to assess financial health.

By managing working capital effectively, businesses can ensure operational efficiency, financial stability, and long-term growth.

Factors Affecting Working Capital

- Cash: Ensure day-to-day expenses while reducing holding costs.

- Inventory: Optimal levels via techniques like JIT or EOQ.

- Receivables: Effective credit policies to balance cash flow and revenue.

- Short-term Financing: Efficient use of credit lines or factoring.

- Business Nature: Different industries require varying levels of WC.

- Market/Demand Conditions: High demand reduces inventory needs.

- Technology: Seasonal businesses may follow production policies accordingly.

- Operating Efficiency: Reducing waste improves WC utilization.

- Price Changes: Rising prices increase WC needs.

Investment in Working Capital

The investment in current assets as working capital depends on various organizational and operational factors. There are no fixed rules, but decisions are influenced by:

- Organizational Objectives

- Trade Policies

- Financial Considerations (Cost-Benefit Analysis)

The level of investment varies based on the following factors:

1. Nature of Industry

- Industries like construction and breweries require large working capital due to long gestation periods.

2. Type of Products

- Consumer durables need higher inventory compared to perishable goods, which have shorter shelf lives.

3. Business Type

- Manufacturing: Requires inventory at three levels—raw materials, work-in-progress, and finished goods.

- Trading: Needs inventory as trading stock.

- Service: Maintains minimal inventory, typically consumables.

4. Volume of Sales

- Higher sales volume often leads to higher receivables and the need for more working capital.

5. Credit Policy

- A liberal credit policy results in higher receivables and increased capital requirements to fund operations.

6. Specific Business Peculiarities

- Some businesses inherently need more working capital:

- Infrastructure companies hold significant inventory as work-in-progress, requiring larger investments.

- Fast food chains need relatively lower working capital due to fast inventory turnover.

Important Financial Ratios

1. Current Ratio

Definition: Measures a company’s ability to pay short-term liabilities with short-term assets.

- Ideal Ratio: Above 1.

- Interpretation:

- High ratio (>2) = Good liquidity, but may indicate idle assets.

- Low ratio (<1) = Risk of insolvency.

Scenarios:

| Scenario | Current Assets | Current Liabilities | Current Ratio | Interpretation |

|---|---|---|---|---|

| I | 600 | 300 | 2:1 | Comfortable zone |

| II | 300 | 300 | 1:1 | Neutral |

| III | 200 | 300 | 0.67:1 | Danger zone |

Scenario 1

For Paying 300 , Resources RS 600

Comfort zone

Current Ratio = 600/300 = 2:1

Scenario II

For Paying 300 , Resources RS 300

Current Ratio = 300/300 = 1:1

Scenario III

For Paying 300 , Resources RS 200

Danger Zone

Current Ratio = 200/300 = 0.67:1

2. Quick Ratio

Assesses a company’s immediate liquidity by excluding less liquid assets like inventory & prepaid expenses.

A ratio close to 1 is generally acceptable; a lower ratio may indicate liquidity issues.

Example:

Company ABC’s Financials

- Cash: $50,000

- Marketable Securities: $30,000

- Accounts Receivable: $40,000

- Inventory: $60,000

- Current Liabilities: $100,000

Step 1: Calculate Quick Assets

Quick Assets=Cash+ Marketable Securities+ Accounts Receivable

50,000+30,000+40,000=120,000

Step 2: Apply the Formula

Quick Ratio=quick asset/current liabilities=120000/100000=1.2:1

A quick ratio of 1.2 means that for every $1 of current liabilities, the company has $1.20 in highly liquid assets to cover those liabilities. A ratio above 1 is generally considered good, indicating the company can meet its short-term obligations without selling inventory.

3. Inventory Turnover Ratio

inventory turnover ratio measures how efficiently a company manages its inventory by showing how many times the inventory is sold and replaced during a specific period. It is calculated as:

Inventory Turnover Ratio = Cost of Goods Sold (COGS)/Average Inventory

Example:

| Scenario | Cost of Sales | Average Inventory | Turnover Ratio | Holding Period |

|---|---|---|---|---|

| I | 120 | 10 | 12 Times | 1 Month |

| II | 120 | 60 | 2 Times | 6 Months |

- Interpretation:

- Higher Ratio: Indicates efficient inventory management and higher profits.

- Lower Ratio: May indicate overstocking or weak sales.

4. Debtors Turnover Ratio

Measures how efficiently a company collects credit sales revenue.

Debtors Turnover Ratio= Annual credit sale/Average debtors

- Net Credit Sales: Total sales made on credit (excluding cash sales and returns).

- Average debtors: The average of the opening and closing balances of debtors during the period.

Average debtors= Opening debtors +Closing debtors/2

| Scenario | Annual Credit Sales | Average Debtors | Turnover Ratio | Payment Period |

|---|---|---|---|---|

| I | 120 | 10 | 12 Times | 1 Month |

| II | 120 | 30 | 4 Times | 3 Months |

- Interpretation:

- Higher Ratio: Fast collections; reflects strong policies.

- Lower Ratio: Slow collections; may cause cash flow issues.

- Scenario 1:- This means the company collects its receivables approximately 12 times a year.

- Scenario 1:- This means the company collects its receivables approximately 4 times a year.

5. Creditors Turnover Ratio

The creditors turnover ratio (also called the accounts payable turnover ratio) measures how quickly a business pays off its creditors or accounts payable during a specific period. It helps assess the company’s efficiency in managing its short-term obligations and maintaining good relationships with suppliers.

Example:

| Scenario | Annual Credit Purchase | Average Creditors | Turnover Ratio | Payment Period |

|---|---|---|---|---|

| I | 120 | 10 | 12 Times | 1 Month |

| II | 120 | 30 | 4 Times | 3 Months |

- Interpretation:

- Higher Ratio: Frequent payments; reflects strong liquidity.

- Lower Ratio: Slow payments; may indicate cash flow problems.

-Note

- Quick Ratio: Liquidity strength; above 1 is good.

- Inventory Turnover: High turnover is efficient; low turnover can hurt profits.

- Debtors Turnover: Faster collection is better; slower collection risks cash flow.

- Creditors Turnover: Frequent payments indicate liquidity; slow payments may raise costs.